4 ways to be ambitious about the EU's new ESG disclosure rules

CSRD, the European Union's new ESG reporting directive, goes into effect in January. Here’s how you can make it not just about compliance, but action. Read More

Let’s have a conversation about CSRD, the European Union’s Corporate Sustainability Reporting Directive that will usher in a new era starting in 2024.

The ambition for CSRD is to transform the way businesses operate to accelerate the transition to a more sustainable and just society. The directive will require more than 60,000 companies in Europe and beyond to disclose, along with annual financial results, information about their environmental and social impacts and governance practices. It also requires companies to define how they will align their business model and strategies to achieve carbon neutrality by 2050. It’s a game changer.

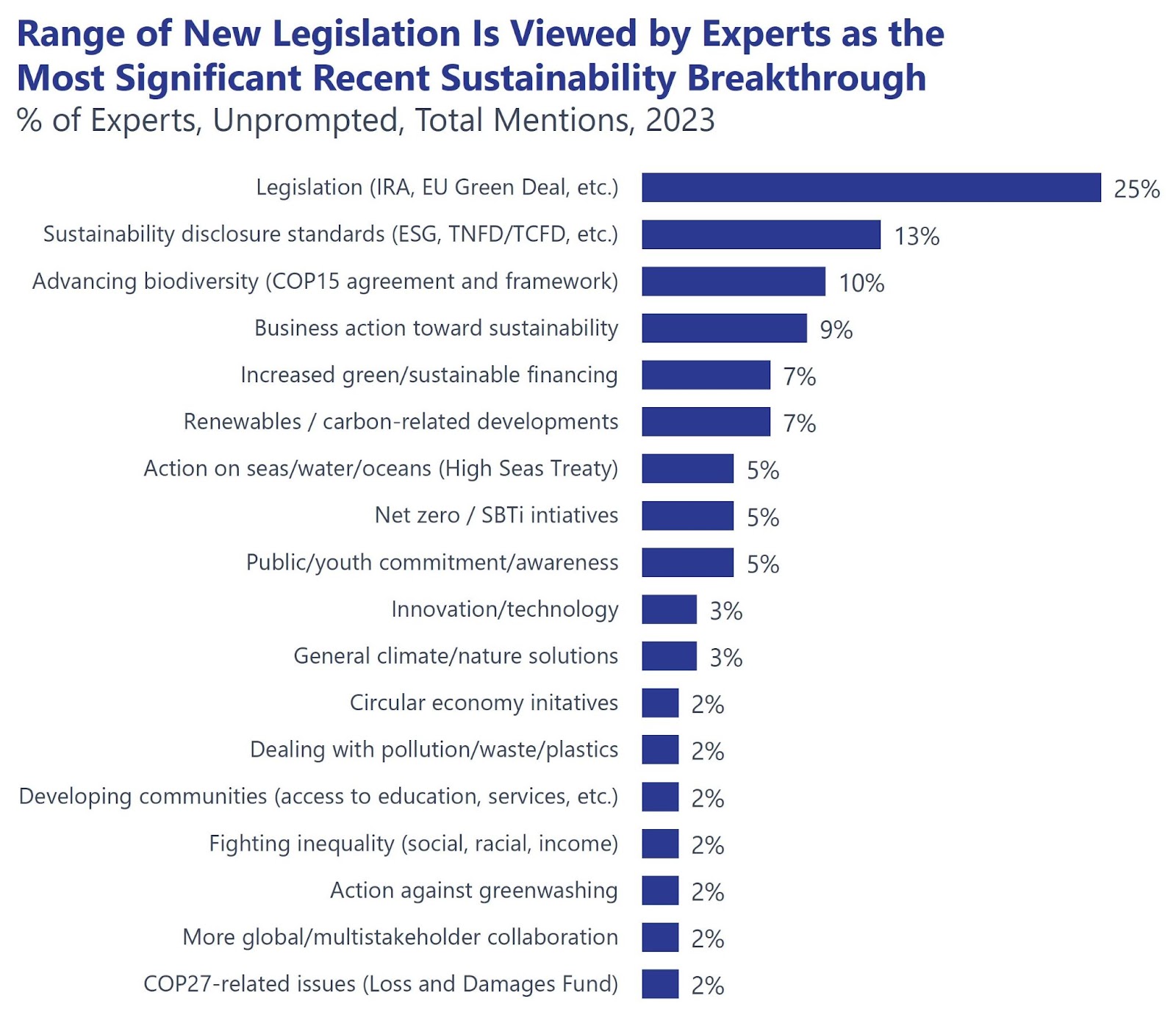

According to the GlobeScan-SustainAbility 2023 Leaders Survey, legislation including CSRD was ranked the most significant sustainability breakthrough of the past year. While ambitious policy that brings sustainability to the forefront alongside finance is what sustainability professionals have wanted for so long, I’ve also found the topic to be quite divisive. When I ask corporate sustainability leaders about how they are preparing for CSRD, I hear two camps: those who lament CSRD as a tick-the-box compliance activity, and those who are convinced CSRD will boost corporate ambition and open up avenues for greater impact.

Perhaps compliance isn’t in opposition with impact. What if we can have and do both?

While there is a level of anxiety that permeates any organization going through change, especially during a rollout, philosopher Peter Nivio Zarlenga reminds us: “Action conquers fear.”

Here are four ways to turn the compliance aspect of CSRD into ambitious action.

Shift resources and start doing

Because CSRD will come into effect in 2024, teams scrambled this year to get prepared. Roles got shuffled around, resources were moved to finance, governance structures were revisited and budgets were reallocated. Many sustainability practitioners talked with me about their concern that their roles could become an accounting function or that their work will focus on looking back on past performance rather than looking forward to what can be done.

Perrine Bouhana, director at global insights advisory firm GlobeScan, sees that practitioners are “putting themselves into the compliance trap if they are only approaching (CSRD) as a tick-the-box activity.” With this in mind, she says: “It will only be different if people approach (CSRD) differently” and as a lever for change.

As we move into the last stretch of the year and the wheels of CSRD are getting into motion, the level of anxiety seems to be receding. A leader at a Scandinavian chemical company saw a shift after the summer break; he told me: “Now that we are starting to talk to our business units, we are seeing a higher level of commitment” and less uncertainty about the path forward. A fellow practitioner from an industrial products manufacturer agrees: “Now that we’re starting to do this, we see that it’s doable. We see that it could push the level of ambition beyond the baseline that CSRD establishes.”

Talk to your suppliers

As they move from internal readiness to engage with external stakeholders, practitioners agree that CSRD will be an impetus to improve supply chain engagement. They also acknowledge that even if corporate ambition is high, the reality of working on the ground with suppliers can be hard. Getting reliable and robust Scope 3 data will continue to be a top challenge. “It can take me a year to get simple data from suppliers, so I’m excited because now I can go back to them with the CSRD imperative,” a practitioner explains.

Look at how your business is affected by sustainability issues, and vice versa

CSRD introduces the concept of “double materiality” to the mainstream and is the first regulation to make it mandatory. Outlined in the European Sustainability Reporting Standards (a provision of CSRD), a double materiality analysis requires companies to assess how their businesses are affected by external sustainability issues (an outside-in lens) and to take it a step further: to consider how their activities impact society and to the environment (inside-out).

In contrast to traditional ESG which is solely risk-focused, Brouhana advises, “We can use double materiality to surface opportunities to create value in ways that we have never seen; moreover, it forces companies to see not only where their negative impacts occur but where they can have positive impacts on the environment as well as society. This alone should energize CSOs who want to be value creators and innovators.”

Strategize with ambition

The way we define sustainability strategies and set ambitious targets will shift with CSRD. With other drivers such as science-based targets, we will have better practices defined and more robust data inventoried. We’ll clarify governance to boost sustainability. We’ll take a systemic look across entire value chains. And we’ll see more internal and external stakeholders integrate sustainability into their roles and mindsets. The next goal setting process will not look like the last round. There will now be a framework to guide companies to focus on where they can have the most positive impacts on the environment and society as well as the bottom line.

How are you framing the CSRD discussion at your company? What are your biggest obstacles internally and externally to prepare? Send me your thoughts, comments or questions at lori@greenbiz.com.