How to make your materiality assessment worth the effort

First, visualize your options. Examples from Unilever and Target. Read More

In the sustainability world, “materiality assessments” are the backbone of reporting. They help identify an organization’s most “material issues” and determine what should be reported. The process of identifying these issues involves reaching out to internal and external stakeholders to get their input. This can be time-consuming, but is a huge opportunity to solicit input on the strategy too.

But many organizations misstep in the process. I hear more stories of materiality assessments that didn’t quite deliver than stories of those that did. Here are some thoughts on improving them.

The key to getting real value out of any materiality assessment is starting with a clear understanding of what information you are looking for. This enables you to ask the right questions, choose the right stakeholders, apply the appropriate methodology and visually present the information effectively to help inform decisions.

Second, materiality assessments can (and should) inform both reporting and strategy.

But the information that is most helpful for strategy development is somewhat different from the information requested for a report. That is fine. It can be presented separately.

There seems to be fundamental confusion about what is “material.”

When asked for guidance on doing a materiality assessment, I commonly hear questions such as: Who are the right stakeholders to engage? What are the right questions to ask? What should the two axis on a materiality matrix be?

Having served as strategy director at Futerra for nearly a year, I now have an answer to factors that generate confusion.

First, the guidance was somewhat ambiguous. The Global Reporting Initiative (GRI) is still the leading organization offering guidance on reporting. Under GRI’s G4/Standards material issues are the topics considered important for “reflecting the organization’s economic, environmental and social impacts” or “influencing the assessments and decisions of stakeholders.” Earlier guidance under G3 left room for various interpretations and reporters are still catching up.

Second, while GRI states there should be a strong link between materiality and strategy, the guidance is focused on what to report on, not what the strategy should be. When organizations use a materiality assessment to guide strategy, the criteria for what is getting prioritized may get mixed up.

What is most “material” from a reporting standpoint may differ from what gets prioritized in a new strategy.

Reporting and strategy development both involve a close look at your material issues and they both benefit from stakeholder consultation. So it makes perfect sense for chief sustainability officers (CSOs) and CSR managers to use one materiality assessment for both purposes.

But reporting and strategy are not the same. There is a fundamental tension between two objectives: deciding what to disclose in your sustainability report (largely backward looking); and deciding what to focus on in your strategy (largely forward looking). The topics prioritized and stakeholders contacted may be different.

From a reporting standpoint, organizations aligning with GRI will want to prioritize topics based on the biggest impacts their organization and the things that influence stakeholder decisions. Current employees, NGOs and investors, for example, can help answer these questions.

From a strategy development standpoint, the goal is to prioritize what an organization can or should do. In this vein, questions about what is within the company’s power to change and what tools, industry groups or new innovations exist to help them do it, can be quite helpful to the action-oriented CSO. These are different questions, and for answers, it can be useful to consult with current employees and people running industry initiatives or innovation labs. In some cases, these might be different people than those who would be consulted for disclosure purposes.

Materiality matrices have evolved

A materiality matrix helps visualize the findings of a materiality assessment. Many variations have emerged to represent what’s important for reporting and what’s important for strategy. This is due to the ambiguity of the previous guidance on materiality and efforts to customize the exercise to meet each company’s individual needs.

Here’s how I categorize them:

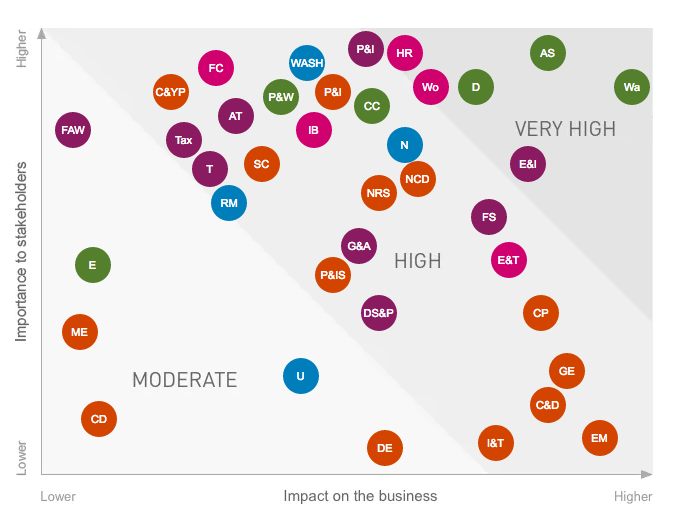

1. The “old school”: Under GRI G3 guidelines, material topics were defined as those that “have a direct or indirect impact on an organization’s ability to create, preserve or erode economic, environmental and social value for itself, its stakeholders and society at large.” With three kinds of value (economic, environmental, social), three entities being affected (business, stakeholders, society) and a two-sided matrix, this left a lot of room for interpretation about how the info should be plotted.

Common ways of plotting include:

Y: Importance to External Stakeholders

X: Impact on Business or Importance to the Business (Internal Stakeholders)

One example is Unilever’s original Sustainable Living Plan material issues matrix below:

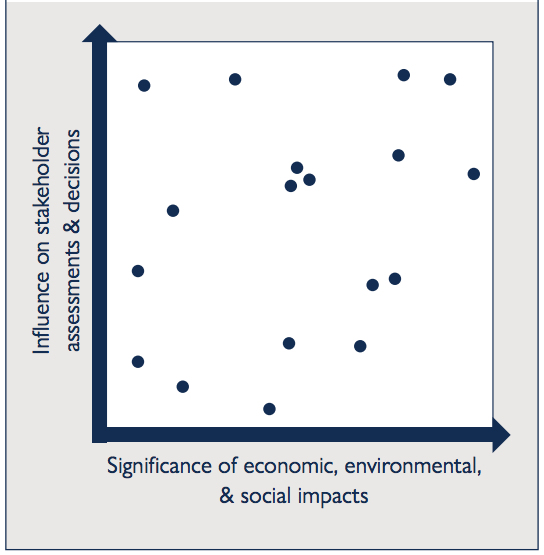

2. GRI’s “new guidance”: Reporting experts such as Elaine Cohen have helped clarify GRI’s G4 Standards. If you choose to use a matrix, it should show what your company’s biggest impacts on the world are, and what investors or employees really want to know when deciding whether to invest or to take a job.

Here is GRI’s example of the visual representation of prioritization topics:

3. The “in-betweens”: All the variations between the new and the old guidance that draw on elements of both.

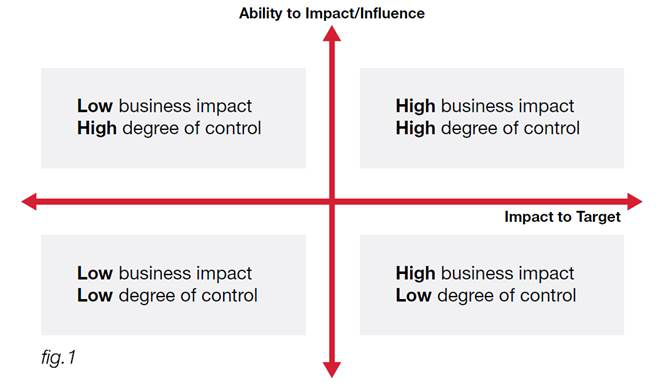

4. The “strategy matrix”: This version of the matrix is a strategy development tool. It does not visualize the information requested by GRI, but focuses on the impacts on the business and what the business can control. Models like this are helpful for strategy, but make it seem as if the materiality assessment process for reporting and for strategy need to be separate, which is not necessary.

They should be integrated as one informs the other:

Y: Ability to impact/influence

X: Impact on the business

Target’s 2016 CSR Report offers an example:

All these materiality matrixes have left people a little confused about what the objective really is, and when that gets muddled, the utility gets lost.

Materiality assessments: one process; separate findings

The most important thing when designing an assessment is to craft questions and select stakeholders to help you make decisions. Be clear about what you want out of each. That’s how you’ll best engage and avoid common mistakes, such as not consulting enough internal stakeholders or industry innovators.

A materiality assessment can be most useful if designed to inform both reporting and strategy. Engaging stakeholders for materiality can be a single exercise, but it helps to keep the insights informing your report separate from those informing your strategy.

Plus, how this information is presented visually is critical. Putting everything on two axes can be overly constraining and mix things up.

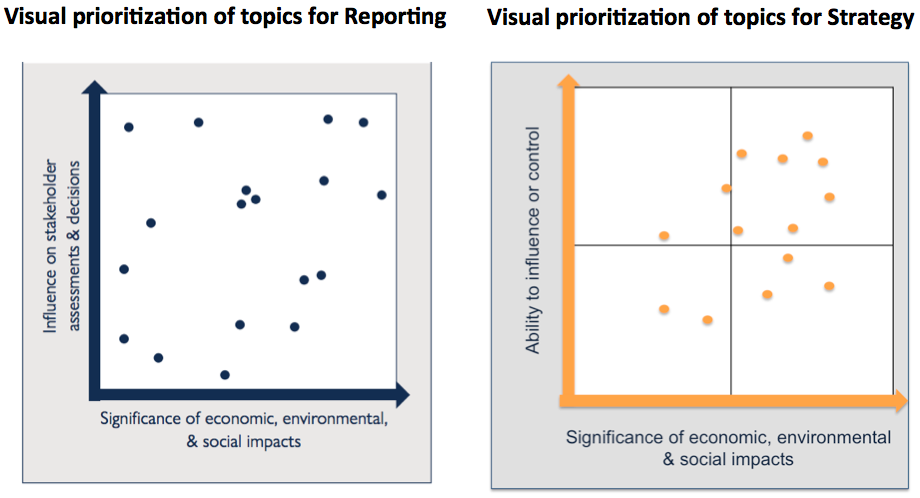

The findings for what to report and for strategy can be charted separately. One chart can follow GRI’s guidance on what to report. Another chart can show information more useful in defining a strategy, such as: “what are the biggest impacts of the business” and its “ability or opportunity to influence or control them.”

Here is a side-by-side visualization:

Other visualization options could also help guide strategy, but impact and control are two powerful driving forces.

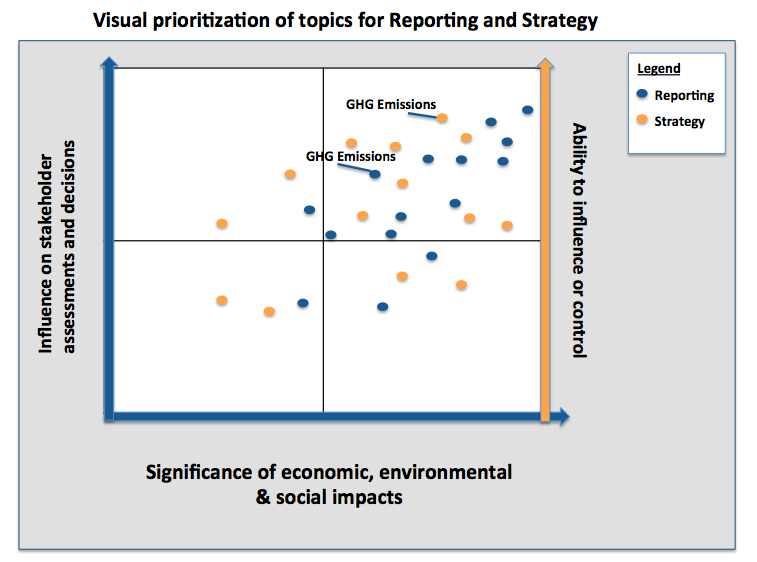

In a final twist, by keeping the X-axis the same, you could even show both reporting priorities and strategy priorities in the same chart by using two Y-axes like this:

Admittedly, this is a lot of information in one place. But putting both reporting and strategy priorities together enables the CSO and other senior leaders to see both backward-looking forward-looking priorities at the same time.

Either way, a well-crafted materiality assessment can inform both reporting and strategy, and help you win over both internal and external stakeholders.