How the EU’s Omnibus package changes CSRD compliance

Spoiler alert: The expected scale back will raise mandatory reporting thresholds and generally lower efficacy of climate-protection efforts. Read More

The European Commission has proposed to scale back the reach and impact of its landmark EU Green Deal, a move causing condemnation among sustainability experts.

“The Commission’s proposal to reopen the CSRD [Corporate Sustainability Reporting Directive] for renegotiation creates legal uncertainty for investors and businesses, and harms the first movers who have already prepared their first sustainability reports or started working towards compliance,” said Nathalie Dogniez, chair of the European Sustainable Investment Forum (Eurosif), in a statement, “The ability of out-of-scope companies to raise finance is likely to be hindered.”

First introduced in 2019, the EU Green Deal — which includes CSRD, Corporate Sustainability Due Diligence Directive (CSDDD) and EU Taxonomy Regulation — didn’t receive much pushback until September, when former Italian Prime Minister Mario Draghi issued “The Future of European Competitiveness” (“Draghi report”). In November, the European Council introduced the Budapest Declaration, which called for a forceful streamlining of regulations. That, along with a general political shift to the right within the EU, led to the release of the Omnibus package.

The new package, expected to be approved sometime this year, drastically reduces the efficacy of the CSDDD (which requires companies to account for the negative impacts of their activities on the environment and humanity), while the EU Taxonomy Regulation (defining which and how a company’s economic activities are environmentally sustainable) remains relatively unchanged.

What followes is a breakdown of the changes proposed for the three packages, and their impact on American companies.

CSRD

The omnibus package proposes a condensing of the thresholds for compulsory company participation.

“[The EU] is going to reset the threshold, and you either have to comply with CSRD or not,” said Maura Hodge, U.S. sustainability leader at KPMG. Hodge added that many companies previously required to report now “won’t have any CSRD requirements.”

Until now, EU-based public companies with more than 500 employees met the threshold. The proposal increases the workforce minimum to 1,000 employees, with an added minimum of $52 million (€50 million) or more in revenue or $26 million (€25 million) or more on their balance sheet.

Additionally, the package exempts small to-medium enterprises (SMEs) — companies with more than 250 employees — from mandated disclosure. This will affect hundreds or possibly thousands of firms.

“Reducing the scope, with even fewer companies included than under the previous NFRD [the EU’s previous disclosure standards], undermines the level playing field needed to achieve sustainable growth,” said Robin Hodess, CEO of the Global Reporting Initiative (GRI), in a press release.

Companies based outside of the EU — many, obviously, in the U.S. — would also see a scale-back in threshold if the Omnibus proposals are adopted.

Before, non-EU based companies — with overall revenue of $156 million (€150 million), and either $41.6 million (€40 million) from an EU branch or a subsidiary that meets the general scoping of CSRD — were held accountable to comply. That would no longer be the case under the proposed revisions. The new threshold would increase to $468 million (€450 million) in revenue and either $52 million (€50 million) from an EU branch or one large EU subsidiary.

These changes, too, would lead to a vast decrease in companies required to disclose emissions.

“The proposal aims to reduce the number of inscope companies by over 80 percent,” said Aleksandra Palinska, executive director at Eurosif, in a release,”Voluntary reporting from companies will not fill this data gap.”

And that’s just the beginning of the changes to CSRD introduced by the omnibus package.

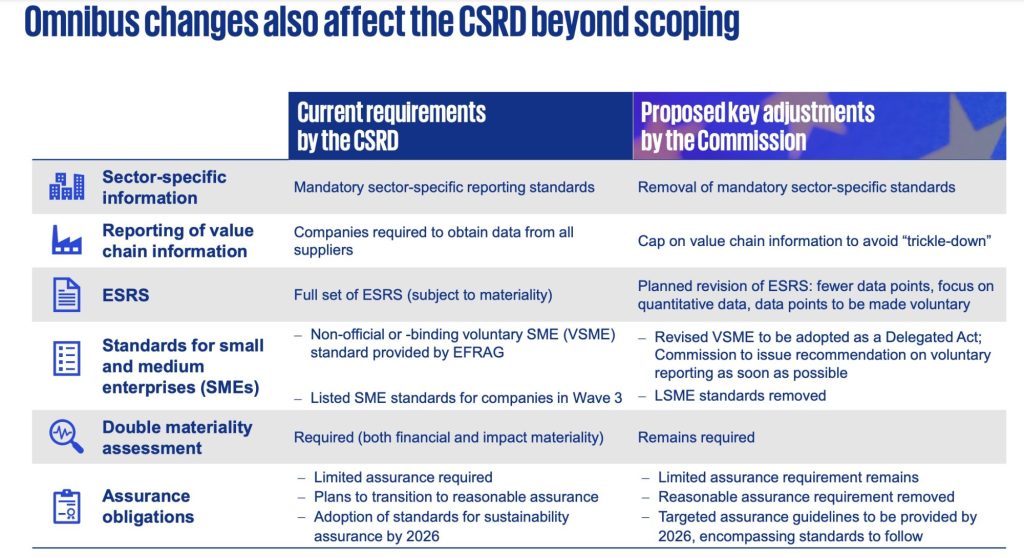

The above graphic from KPMG summarizes the difference between the current CSRD requirements and the proposed revisions of the package. Every major step of CSRD is scaled back, save for the double materiality assessment. This means that companies, both those within the EU and otherwise, would still be required to evaluate and report their financial impact from sustainability measures, along with the company’s impact on society and the environment.

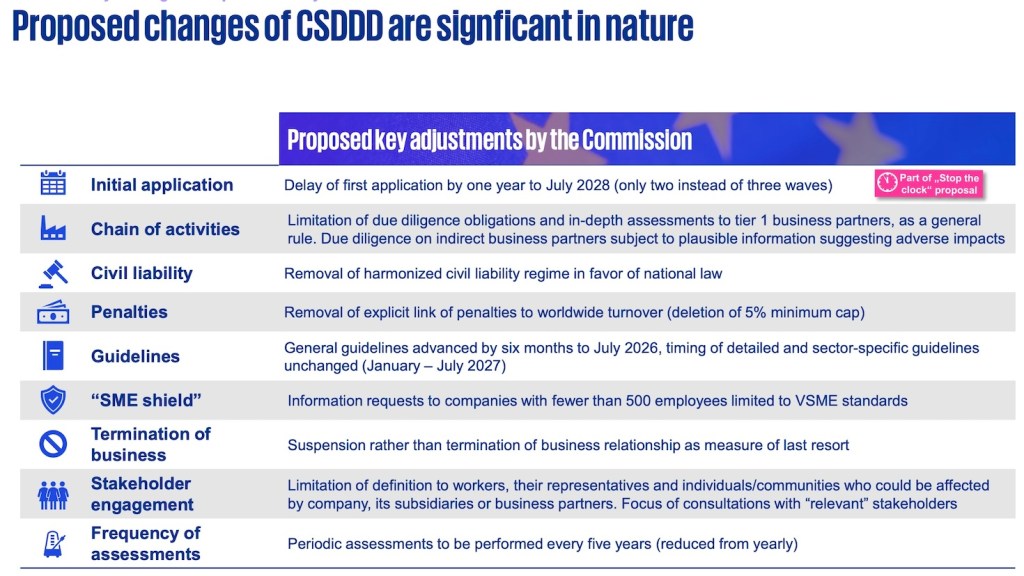

CSDDD

CSDDD was originally designed to assess risk to humanity and the environment across a company’s value chain. The proposed update would lessen the due diligence obligations designed to calculate that risk for all direct stakeholders in the chain, and assessments for indirect businesses would now be optional.

The proposal also completely removes EU oversight of civil liabilities — the potential for a company to compensate a person for damage that results from its CSRD noncompliance — and instead places it at the national level, and at each country’s discretion.

“Stripping due diligence beyond direct suppliers, scrapping stakeholder engagement and eliminating civil liability give corporations a free pass to operate without consequences,” said Nele Meyer, director of the European Coalition for Corporate Justice, in a statement.

EU Taxonomy

The EU Taxonomy escaped relatively unscathed from the Omnibus revisions.

Despite calls to make taxonomy voluntarily, it would remain a compulsory addition to a corporation’s CSRD report. Of course, as CSRD compliance is watered down, so too would be taxonomy’s coverage.

What’s next

The EU still needs to approve the Omnibus package, starting with a public commenting period and ending with the European Parliament and Council’s vote. But companies, particularly those based in the U.S., should not wait to act.

Advised Hodge: “Continue to move forward on climate, particularly preparing your Scope 1, 2, and 3 greenhouse gas inventory and identifying and mitigating climate risks. State laws continue to stand.”

Hodge recommended that all companies should immediately identify how they are affected by the proposed thresholds and how they “might influence your reporting strategy.” Smaller companies in both the U.S. and EU may find themselves exempt from CSRD reporting — or just with a postponed timeline.

Hodge also offered advice to companies that may soon find themselves with a surplus of funds previously marked for corporate disclosure.

“Think about how you might redeploy your reporting budget toward strategic value-add projects,” she said, “like technology solutions or decarbonization efforts in the current year.”