How ‘Scope 4’ emissions can help and hinder sustainability efforts

Companies seeking to report “avoided emissions” will need to tread carefully through the greenwash minefield. Read More

How do you measure something that never existed?

Companies may soon be posing this Zen koan to address the emerging accounting concept called Scope 4. It refers to “avoided emissions” of the greenhouse variety.

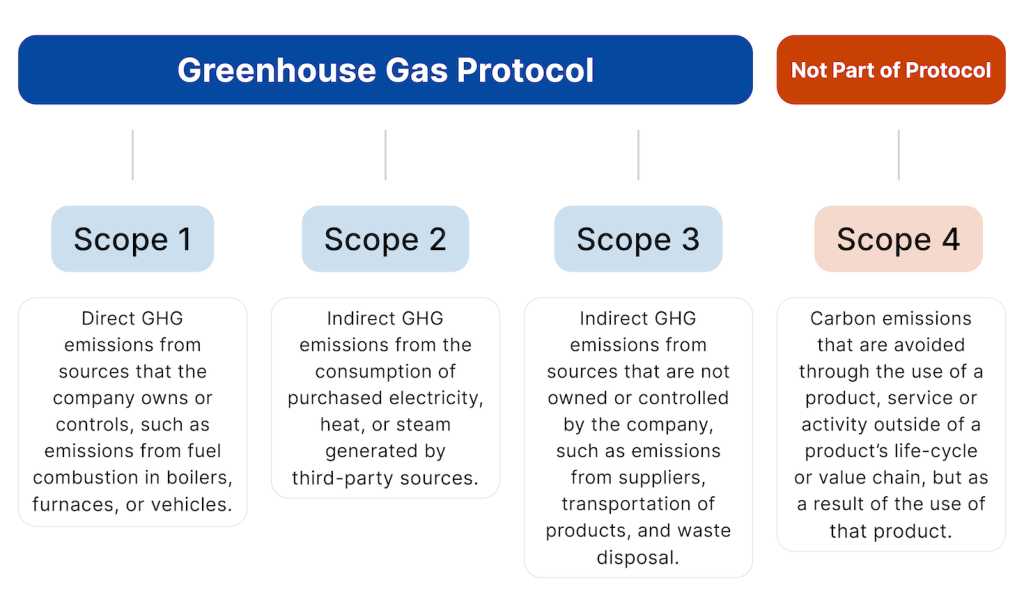

In simple terms, Scope 4 refers to greenhouse gases never emitted due to a product’s cleaner production or attributes. Or, more precisely, “the difference in total lifecycle GHG emissions between a company’s product and some alternative product that provides an equivalent function,” according to the World Resources Institute. “Product,” in this case, includes both goods and services.

So, an electric vehicle replacing a petroleum-powered one; steel produced in a factory powered by hydrogen instead of fossil fuels; a flight powered in part with sustainable aviation fuel; or a Zoom meeting that obviates the need to travel, to cite a few examples.

Like most carbon accounting, it’s complicated.

A lack of standards

By virtue of its name, Scope 4 would appear to be part of the Greenhouse Gas Protocol, adopted two decades ago by the World Resources Institute and the World Business Council for Sustainable Development and generally accepted as the gold standard for greenhouse gas accounting and reporting. Scopes 1, 2 and 3 are now so ingrained in business argot that CEOs routinely refer to them in public speeches.

But Scope 4 isn’t part of that protocol — at least, not yet. In fact, there are few agreed-upon standards for what constitutes an “avoided emission.”

This isn’t the first framework designed to enable companies to tout the environmental benefits of products and services. Life-cycle assessments, or LCAs, have long been used to compare one product’s impact to another’s. Environmental product declarations enable producers to make complex LCA data more accessible to customers. And there’s the concept of a “handprint” — the opposite of a footprint — yet another articulation of the positive environmental impacts of a product, service or company.

While each has its niche, Scope 4, if only by virtue of its official-sounding name and carbon focus, seems best positioned to become a widespread means for companies to measure and communicate their contributions to addressing the climate crisis.

That could be a big problem.

Scope 4 is rife with potential for companies to misstate the benefits they engender. In the absence of credible frameworks or guidelines, it is likely that many companies will report information that’s inaccurate, misleading or simply debatable.

“There is a lot of potential for greenwashing,” Jacob Madsen, senior director for carbon solutions at the carbon-accounting software firm Persefoni, told me. Madsen has spent nearly 30 years working in LCA frameworks and metrics and knows a bit about the many ways the same piece of data can be interpreted.

Accurately reporting Scope 4, he said, will require companies to fully understand how their products compare to competitors’ and to the status quo — that is, to conduct an LCA, which can be complicated, expensive and subjective.

The complexities of measuring avoided emissions will be familiar to those who have engaged with carbon accounting. Among them: boundaries (what specific part of a product’s production and use is the company claiming as “avoided”?), additionality (is the company claiming the benefit of something that might have happened anyway, such as a Zoom meeting instead of a business trip?) and double counting (is more than one entity claiming the same avoided emissions?).

Countdown to COP 16: Key Strategies for Engaging with the Biodiversity Conference

Consider a hypothetical. Your company puts solar panels on its roof, reducing the need for fossil energy and the resulting emissions. Who gets to claim the avoided emissions — your company, the firm that manufactured the panels or the firm that sold and installed them? Or maybe the electric utility or government agency that provided financial incentives that made it all affordable? And do the claimed benefits end at your facility, or do they extend to the downstream products and services that facility provides to customers?

Without definitive rules, accurately measuring avoided emissions could be tricky, to say the least.

Show the math

At minimum, Scope 4 can bring rigor and transparency to the types of marketing claims companies already make. For example, any company touting that a product’s climate benefits are “the equivalent of taking [insert number] cars off the road” is claiming avoided emissions. So is a firm that claims a product’s energy savings are sufficient to power [insert city or nation] for [insert length of time].

Under Scope 4, companies will need to show the math.

Such challenges aside, a few companies are dipping their toes into Scope 4 waters. Among them: Panasonic, PG&E and Schneider Electric.

At PG&E, the California-based investor-owned utility, Scope 4 represents “a collection of measures,” according to Christopher Benjamin, its director of corporate sustainability. For example, it includes customer energy-efficiency programs using a measurement methodology approved by the California Public Utility Commission. It also includes the utility’s electric vehicle adoption program, which aims to encourage drivers to switch from gas-powered vehicles, and industrial programs that help companies shift to more efficient and cleaner-running equipment.

PG&E always puts “Scope 4” in quotes, Benjamin said, “because we recognize that it’s not an official category and doesn’t have an official standard.”

Why bother at all? “It’s a way of quantifying the effort and level of ambition that we are putting into helping our customers make this transition,” he told me.

Scope 4 is unquestionably compelling: Who wouldn’t prefer to talk about the good they do as opposed to being less bad? That will likely make it attractive to corporate PR and marketing departments. But it can also be risky. For example, companies seeking to subtract avoided emissions from their actual emissions to claim a smaller net footprint should expect to see pushback from activists, investors, regulators and customers.

The ultimate question is whether companies currently grappling with the complexities of Scopes 1, 2 and 3 will see Scope 4 as a simpler means to tout their climate leadership, and whether avoided-emissions claims are verifiable and represent bona fide emissions reductions.

Or whether “avoided emissions” becomes yet another sustainability term that is ill-defined — and, ultimately, misused, overused and abused.