How to navigate all those certifications in the voluntary carbon market

An unregulated field has become a crowded one. Read More

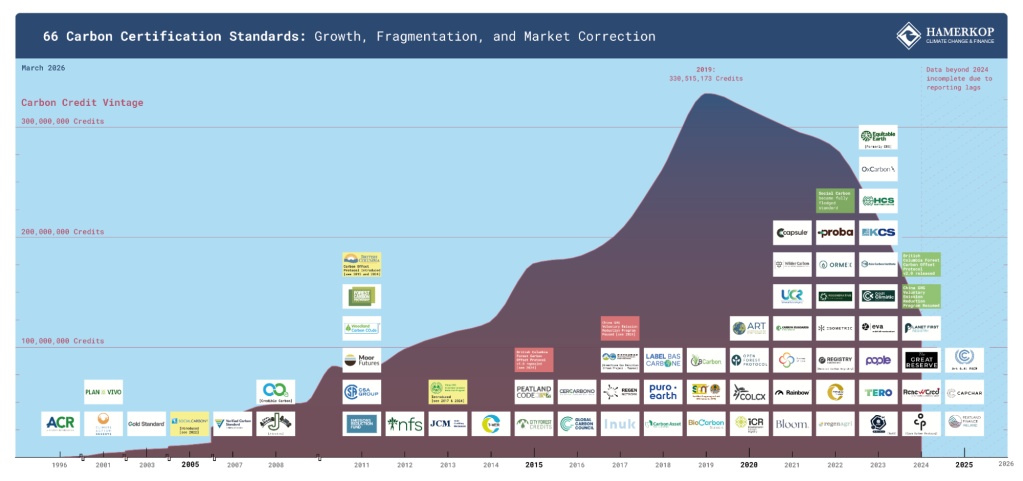

- Climate consultancy Hamerkop identified 66 organizations that are issuing carbon credits.

- The number of competing certifications surged after 2020, but growth has slowed recently.

- Some newer certifications are building a reputation for quality.

Buyers in the voluntary carbon market often find it challenging to differentiate between higher- and lower-quality credits. One cause might be the range of organizations issuing carbon credits: According to a count released this week, at least 66 entities are currently doing so.

The list includes well-established players that helped build the market, including Verra and Gold Standard, alongside notable new entries, such as Puro and Isometric, as well as a long tail of smaller and lesser-known issuers. The field is crowded in part because it’s unregulated; any organization can create standards and issue credits. The result is a confusing field of issuers that at first glance appear similar, but in practice operate to very different levels of rigor.

Sixty-six certifications actually represent a slowdown in growth, according to data from Hamerkop Climate Impacts, the climate consultancy behind the count. New certifications surged after 2020 as an increasing number of companies set net-zero targets and specialist issuers sprung up to focus on carbon removal, nature-based solutions and other niches. The past two years have been relatively quiet by comparison.

Launches of new carbon credit certifications

“The slowdown in new launches in 2024 and 2025 reflects a shift in market conditions,” said Olivier Levallois, Hamerkop’s founding director. “Confidence in the voluntary carbon market has been affected by scrutiny around credit quality. As a result, the market has become more cautious, and the business case for launching new standards has weakened.”

Navigating the market

To navigate this confusing territory, Levallois suggests the following:

- Caution is warranted. Watch for standards that lack a clear track record, including those that have been operational for several years but have seen limited uptake or issuance. This can indicate challenges around market acceptance or robustness.

- Governance is critical. Standards that are closely linked to project developers or commercial interests may raise questions about conflicts of interest.

- Transparency is key. Check that methodologies, validation processes and issuance data are publicly available and subject to scrutiny.

- Not all new or small standards should be dismissed. Some are gaining traction in specific segments. Equitable Earth, for instance, positions itself as providing higher integrity and more equitable approaches to reducing deforestation.

“Certifications are just one layer in what is now a four- or five-layer quality assurance stack: registries, third-party verifiers, standards bodies like ICVCM, ratings agencies, and buyer-side diligence all sit on top of one another,” said Sanna O’Connor-Morberg, director of strategy and markets at Carbon Direct, a climate consultancy. “The proliferation of certifications is the most visible piece, but it’s just the tip of the iceberg. Even with all those layers, low-quality projects remain abundant. That tells you the system isn’t yet calibrated to fail in the right direction.”